New Trump Kids Accounts

The new Trump accounts provide another way to save for a child's retirement. Here's how they'll work and why they may be worth considering.

As part of the One Big Beautiful Bill Act passed in July 2025, new Trump accounts give eligible American children born between January 1, 2025, and December 31, 2028, a one-time deposit of $1,000 from the U.S. government. They also allow parents and others to contribute a total of up to $5,000 annually in after-tax dollars.

The Government contribution is a valuable benefit, but the removal of the earned-income requirement may be the bigger development — meaning parents can begin funding a child’s retirement savings from birth rather than waiting until the child has a job. That said, other account types may still be a better fit depending on your situation

Eligibility

- An account can be established for any child with a Social Security number who is age 17 or younger for the entire calendar year in which the account is opened.

Government contribution

- Only U.S. citizens who have a Social Security number and are born between 2025 and 2028 are eligible for the $1,000 deposit.

- The $1,000 deposit doesn’t count toward the $5,000 annual contribution limit.

Contribution limits

- Annual contributions are capped at $5,000 in 2026 and are indexed to inflation beginning in 2028.

- A parent’s or child’s employer may contribute up to $2,500 in 2026 (indexed to inflation beginning in 2028)—which doesn’t count toward the employee’s taxable income but does count toward the annual limit.

- Federal, state, and local governments, along with charities, can contribute tax-free to a child’s account without impacting the annual limit.

- In the year the child turns 18, the account becomes subject to the same contribution rules governing traditional IRAs.

Investments

- Contributions must be invested in funds that track a qualified U.S. stock index, do not use leverage, and do not have annual fees and expenses of more than 0.1%. (A qualified U.S. stock index is the S&P 500® or any other index that’s composed primarily of the stocks of U.S.-based companies and for which regulated futures contracts are traded on a qualified board or exchange. Industry- or sector-specific indexes do not qualify.)

Withdrawals

- The money generally can’t be withdrawn before the account owner turns 18.

- When the child turns 18, the account becomes subject to the same withdrawal rules governing traditional IRAs.

Taxes

- While personal contributions aren’t tax-deductible, neither are they subject to federal taxes when withdrawn. That said, withdrawals of any earnings or pretax amounts will generally be taxed as ordinary income.

- Early-withdrawal penalties apply for distributions taken before age 59½ unless used for qualified expenses, such as certain higher education costs or the purchase of a first home (up to $10,000).

Additional Details

- Any amount gifted to a child from an individual, no matter the account, may be subject to the applicable gift tax exclusion and may need to be reported on IRS Form 709. State rules may vary.

Sources: One Big Beautiful Bill Act, 2025. | The Council of Economic Advisers, “Trump Accounts Give the Next Generation a Jump Start on Saving,” whitehouse.gov, 08/29/2025.

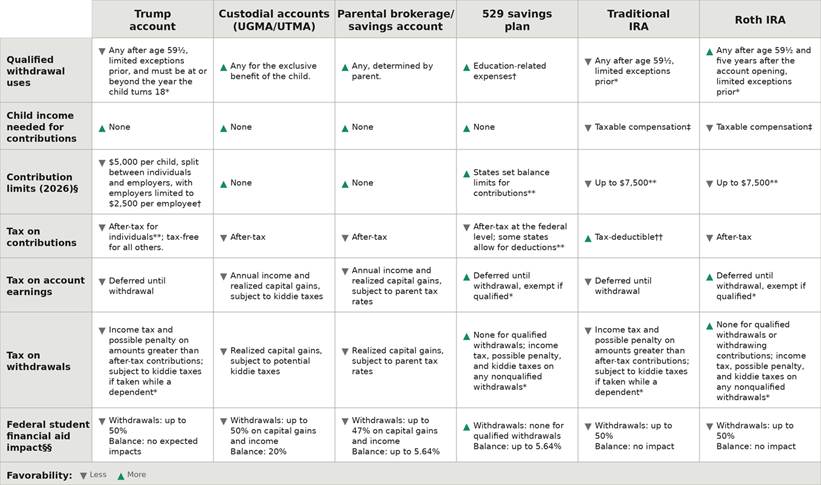

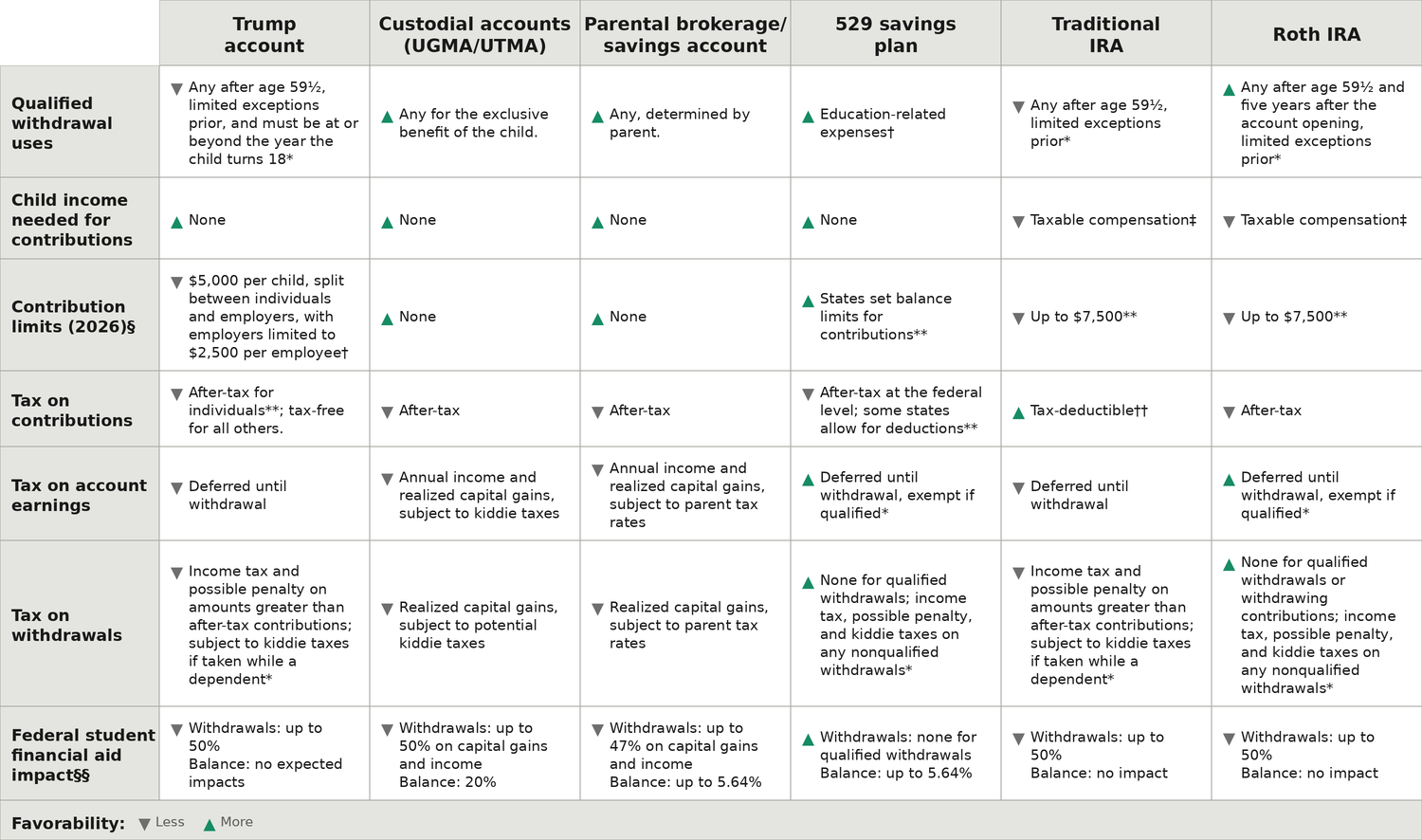

Comparing key features of popular accounts for child savings

{kind=link}

* Withdrawals from a Trump account generally align with IRAs beginning January 1 in the year the child turns 18. More information can be found in IRS Notice 2025-68 for Trump accounts and IRS Publication 590-B for IRAs.

† More information on qualified educational withdrawals can be found in IRS Publication 970. Not all states align with federal definitions for qualified expenses. For more information about any 529 savings plan, contact the plan provider to obtain a Program Description.

‡ Taxable compensation (earned income) must be received by the child for contribution eligibility. A description can be found in IRS Publication 590-A.

§ Any amount gifted to a child from an individual, no matter the account, may be subject to the applicable gift tax exclusion and may need to be reported on IRS Form 709. State rules may vary.

¶ The employer limit is per employee. More information can be found in IRS Notice 2025-68.

** Once the balance limit is reached, contributions are suspended until the balance drops below the limit. State deductions may also be subject to later recapture if funds are used for nonqualified purposes. For more information about any 529 savings plan, contact the plan provider to obtain a Program Description.

†† Contributions and deductibility are subject to certain income limitations that can be found in IRS Publication 590-A. Given dependent standard deduction rules, there may not be a tax advantage in making traditional IRA contributions for a dependent child unless they earn more than the single filer standard deduction.

‡‡ It is not clear at this time whether Trump account contributions from individuals, other than the child, may be eligible for the annual gift tax exclusion. If not, then the donor would need to file a gift tax form, IRS Form 709, and taxes may be due, subject to applicable limits.

§§ Weightings shown represent the portion of a withdrawal or balance that may result in a reduction of federal student financial aid. Weightings shown using Formula A for a Dependent Student based on 2026–2027 FAFSA guidelines. College Scholarship Service (CSS) Profile schools may use alternative weightings.

Notes: All information considers the sources listed and is focused on tax and federal student financial aid impacts only. The figure is for illustrative purposes based on publicly available information on Trump accounts and other accounts as of February 10, 2026. This information is for general guidance only and does not take into consideration personal circumstances or other factors that may be important in making investment decisions.

We recommend consulting a financial or tax advisor before investing.

Source: Vanguard.